Asymmetric Information and Adverse selection, Problems of individual insurance?

Hellow guys, Welcome to my website, and you are watching Asymmetric Information and Adverse selection, Problems of individual insurance?. and this vIdeo is uploaded by Insurance help at 2016-06-16T03:24:10-07:00. We are pramote this video only for entertainment and educational perpose only. So, I hop you like our website.

Info About This Video

| Name |

Asymmetric Information and Adverse selection, Problems of individual insurance? |

| Video Uploader |

Video From Insurance help |

| Upload Date |

This Video Uploaded At 16-06-2016 10:24:10 |

| Video Discription |

Asymmetric Information and Adverse selection

Introduction

Economics 306 – build models of individual, firm and market behavior

Most models assume actors fully informed about the market specifics

Know prices, incomes, market demand, etc.

However, many markets do not have this degree of information

Look at the role of ‘imperfect information’

This is more than just ‘uncertainty’ – we’ve already dealt with that issue

Problem of asymmetric information

Parties on the opposite side of a transaction have different amounts of information

Health care ripe w/ problems of asymmetric information

Patients know their risks, insurance companies may not

Doctors understand the proper treatments, patients may not

Problem of individual insurance

Consider situation where people can purchase individual health insurance policy

Problem for insurance companies

They do not know who has the highest risk of expenditures

People themselves have an idea whether they are a high risk person

Asymmetric information

Can lead to poor performance in the private insurance market

Demonstrate in simple numeric example the problem of ‘adverse selection’

Definition: those purchasing insurance are a non-representative portion of the population

This section

Outline problem of asymmetric information and adverse selection

Focus on

How selection can impact market outcomes

‘How much’ adverse selection is in the market

Give some examples

How can get around

Why EPHI might help solve AI/AS

Focus in this chapter will be on the consumer side – how their information alters insurance markets

Are some other examples

How doctors’ asymmetric information might alter procedure

Will save for another time

Keep focused on insurance

Market for Lemons

Nice simple mathematical example of how asymmetric information AI can force markets to unravel

Attributed to George Akeloff, Nobel Prize a few years ago

Good starting point for this analysis, although it does not deal with insuance

Problem Setup

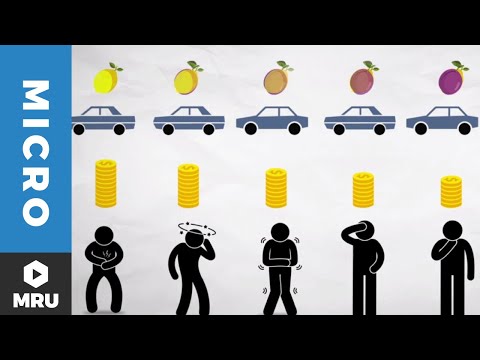

Market for used cars

Sellers know exact quality of the cars they sell

Buyers can only identify the quality by purchasing the good

Buyer beware: cannot get your $ back if you buy a bad car

Two types of cars: high and low quality

High quality cars are worth $20,000, low are worth $2000

Suppose that people know that in the population of used cars that ½ are high quality

Already a strong unrealistic assumption

One that is not likely satisfied

Buyers do not know the quality of the product until they purchase

How much are they willing to pay?

Expected value 1/2$20K + 1/2$2K $11K

People are willing to pay $11K for an automobile

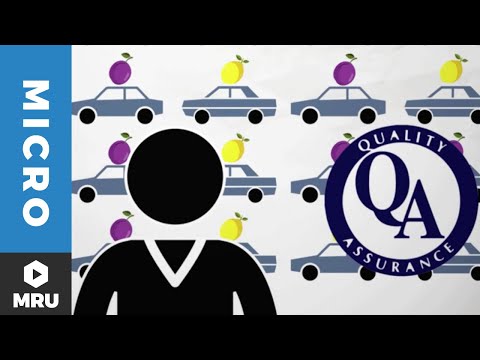

Would $11K be the equilibrium price?

Who is willing to sell an automobile at $11K

High quality owner has $20K auto

Low quality owner has $2K

Only low quality owners enter the market

Suppose you are a buyer, you pay $11K for an auto and you get a lemon, what would you do?

Sell it for on the market for $11K

Eventually what will happen?

Low quality cars will drive out high quality

Equilibrium price will fall to $2000

Only low quality cars will be sold

Some solutions?

Deals can offer money back guarantees

Does not solve the asymmetric info problem, but treats the downside risk of asy. Info

Buyers can take to a garage for an inspection

Can solve some of the asymmetric information problem

Insurance Example

All people have $50k income income

When health shock hits, all lose $20,000

Two groups

Group one has probability of loss of 10%

Group two has probability of loss of 70%

Key assumption: people know their type

EIncome1 0.950K + 0.130K$48K

EIncome2 0.350K + 0.730K$36K

Suppose uY0.5

Easy to show that

EU1 .950K0.5 + .130K0.5 218.6

EU2 .350K0.5 + .730K0.5 188.3

What are these groups willing to pay for insurance?

Insurance will leave them with the same income in both states of the world

In the good state, have income Y, pay premium Prem, UY-Prem0.5

In the bad state, have income Y, pay premium P, experience loss L, receive check from insurance for L

Uw/insurance Y-Prem0.5

Group 1: Certain income that leaves them as well off as if they had no insurance

U Y-Prem0.5 218.6, so Y-Prem 218.62 $47,771

Group 2: same deal

U Y-Prem0.5 188.3, so Y-Prem 188.32 $35,467 |

| Category |

People & Blogs |

| Tags |

insurance | insurance policy | nonprofit | health insurance | insurance auto auction | insurance adjuster | insurance age | insurance act | insurance agent salary | insurance agent | Asymmetric Information and Adverse selection | Problems of individual insurance? |

More Videos